This example illustrates a single-entry system used by Henry Brown, who is the sole proprietor of a small automotive body shop. Henry uses part-time help, has no inventory of items held for sale, and uses the cash method of accounting. These sample records should not be viewed as a recommendation of how to keep your records. They are intended only to show how one business keeps its records and to make you familiar with some of the terminology used in accounting.

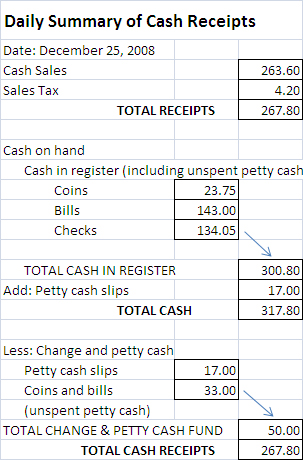

1. Daily Summary of Cash Receipts

This summary is a record of cash sales for the day. It accounts for cash at the end of the day over the amount in the Change and Petty Cash Fund at the beginning of the day. Henry takes the cash sales entry from his cash register tape. If he had no cash register, he would simply total his cash sale slips and any other cash received that day.

Petty cash fund. Henry uses a petty cash fund to make small payments without having to write checks for small amounts. Each time he makes a payment from this fund, he makes out a petty cash slip and attaches it to his receipt as proof of payment. He sets up a fixed amount ($50) in his petty cash fund. The total of the unspent petty cash and the amounts on the petty cash slips should equal the fixed amount of the fund. When the totals on the petty cash slips approach the fixed amount, he brings the cash in the fund back to the fixed amount by writing a check to 'Petty Cash' for the total of the outstanding slips. This restores the fund to its fixed amount of $50. He then summarizes the slips and enters them in the proper columns in the monthly check disbursements journal.